How Lenders Calculate Your Maximum Home Purchase Price

When preparing to purchase a home, determining a target property price can feel overwhelming. Many buyers make the mistake of choosing a price range first, then seeking a mortgage that matches it. Underwriters do the opposite. They evaluate your current income stability, liquid assets, and long-term liabilities, and then use mathematical formulas to establish a maximum monthly payment threshold.

By understanding how these limits are determined, you can prepare your finances to maximize your purchasing budget or identify a comfortable monthly liability that does not strain your lifestyle.

Deconstructing the 28/36 Debt-to-Income Rule

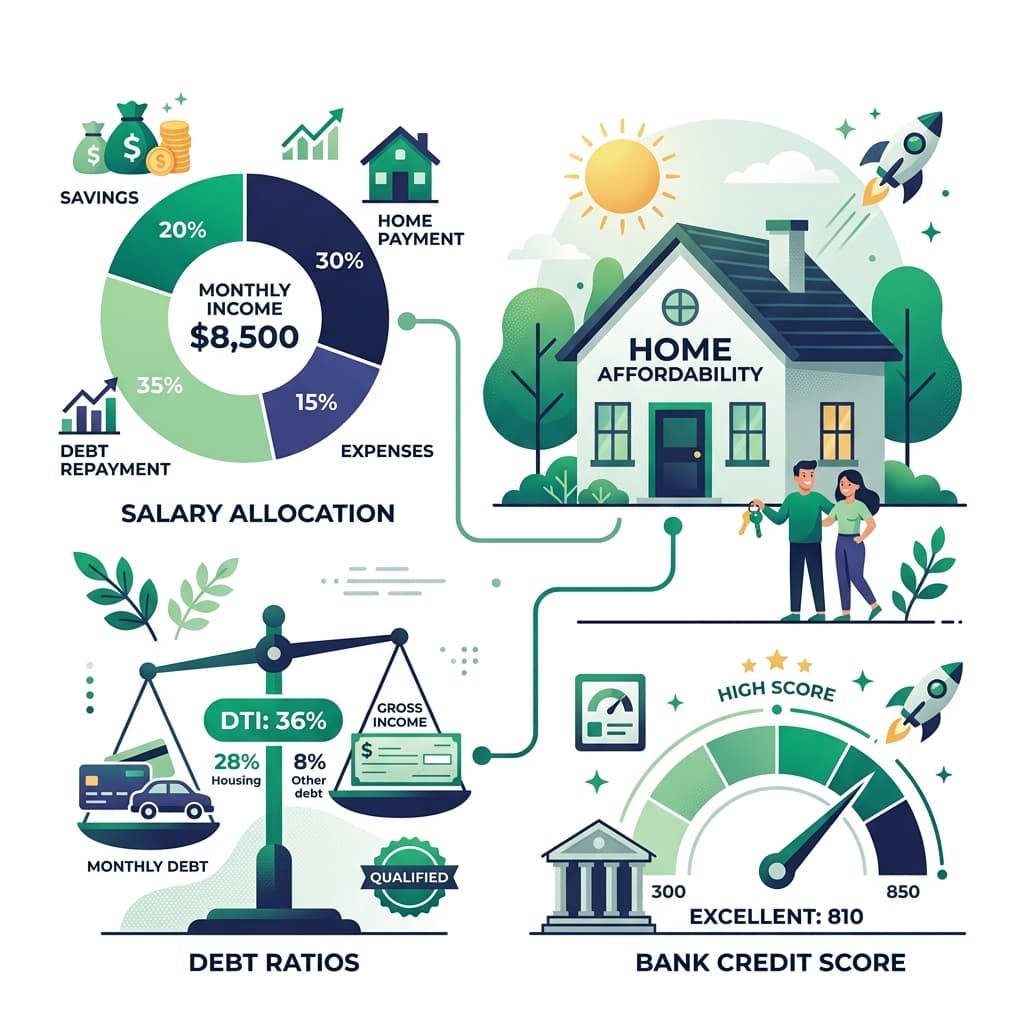

Lenders assess your borrowing risk using two primary ratios collectively known as the 28/36 rule. These ratios represent the maximum percentage of your gross (pre-tax) income that can be allocated to debt service.

The Front-End Ratio (28%)

The Front-End Ratio focuses exclusively on housing costs. Under this rule, your total monthly housing liability (PITI: Principal, Interest, property Taxes, homeowners Insurance, and PMI) must not exceed 28% of your gross monthly income.

The Back-End Ratio (36%)

The Back-End Ratio evaluates your total debt load. Under this rule, your total housing liability plus all other monthly recurring debts (such as car payments, student loans, minimum credit card payments, and child support) must not exceed 36% of your gross monthly income.

If you have low monthly debts, your affordability will be limited by the front-end (28%) housing ratio. However, if you carry substantial student loan debt or a high car payment, the back-end (36%) ratio will be the constraining factor, significantly reducing the amount you can borrow.

The Home Affordability Formulas

Lenders calculate your maximum allowable monthly housing payment (PITI) by taking the minimum of two different limits. The formula uses your Gross Monthly Income (GMI) and Monthly Debts (MD):

Under standard banking guidelines, the Allowable Monthly PITI represents the absolute maximum amount a borrower can allocate to housing costs each month. If your Monthly Debts (credit cards, student loans, car notes) are high, the Back-End Limit will constrain your home purchase capacity.

Reverse Engineering Affordability: From Monthly Limit to Purchase Price

Once underwriters calculate your maximum monthly housing payment limit (the lower of the 28% and 36% targets), they work backward to determine the maximum loan size. This calculation relies on:

- Interest Rate: Higher interest rates increase the proportion of the payment going to interest, which lowers the principal amount you can borrow.

- Down Payment: Your down payment is added directly to the calculated loan limit to establish the maximum purchase price. Every dollar saved for a down payment increases your purchase limit dollar-for-dollar.

- Local Taxes and Insurance: Because property taxes and insurance are built into the monthly payment limit, regions with high local tax rates reduce the amount of income available for principal and interest payments, resulting in lower home budget limits.

How Mortgage Interest Rates Affect Your Purchasing Power

Mortgage interest rates have a significant impact on your overall home buying budget. Because affordability is calculated based on a fixed monthly payment limit, higher interest rates decrease the proportion of that payment that goes toward reducing your loan's principal balance.

For example, if you qualify for a maximum monthly principal and interest payment of $2,000, a 1% increase in interest rates (e.g., from 6.0% to 7.0%) can reduce your home purchasing budget by approximately 10%. Over a 30-year loan term, this slight rate change can mean losing tens of thousands of dollars in home buying power, demonstrating why optimizing your credit score and shopping for the best loan rates is a critical step in the home buying process.

Tactical Actions to Optimize Your Borrowing Capacity

If your affordability limits are lower than your target housing market requires, you can take several strategic steps to improve your debt-to-income (DTI) metrics before submitting a formal application:

- Pay Off Small Balances: Focus on eliminating credit card balances or car loans with less than 10 months of remaining payments. Eliminating these monthly payments completely reduces your recurring monthly debts, directly boosting your back-end DTI space.

- Increase Your Down Payment: Saving a larger down payment reduces your loan-to-value (LTV) ratio. If you can reach a 20% down payment, you avoid PMI fees entirely, which frees up additional monthly budget to support a higher principal loan.

- Optimize Your Credit Score: A higher credit score qualifies you for lower interest rates. A difference of just 1% in your mortgage interest rate can translate to thousands of dollars in increased borrowing capacity or lower monthly payments.

- Shop for Home Insurance: While property taxes are generally fixed by location, homeowners insurance rates vary. Comparing policies and choosing a competitive insurer helps minimize your monthly insurance costs, freeing up additional budget for principal payments.

Home Affordability FAQ

The 28/36 rule is a standard lending guideline. It states that a household should spend a maximum of 28% of its gross monthly income on housing expenses (front-end ratio) and a maximum of 36% on total debt service, including housing expenses and other recurring debts like credit cards, car loans, and student loans (back-end ratio).

A larger down payment directly increases your home buying budget dollar-for-dollar. Additionally, if your down payment is at least 20% of the purchase price, you avoid paying Private Mortgage Insurance (PMI) fees, which reduces your monthly housing payment and allows you to afford a higher principal loan.

PITI stands for Principal, Interest, property Taxes, and homeowners Insurance. These four components make up your monthly housing payment. If applicable, PITI also includes private mortgage insurance (PMI) and homeowners association (HOA) fees.

Recurring monthly liabilities directly reduce the amount of income available for your housing expenses under the back-end DTI limit (36%). For instance, a $500 monthly car payment reduces the monthly mortgage payment you qualify for by exactly $500, which can lower your borrowing capacity by tens of thousands of dollars.

A Conservative limit (28/36 DTI) is recommended for most buyers because it leaves plenty of room in your budget for savings, travel, and unexpected expenses. A Stretch limit (up to 45% DTI) might be acceptable if you have strong credit, stable career prospects, low expenses, or significant cash reserves, but it increases the risk of becoming "house poor."