Understanding Amortization Schedules & Equity Curves

When you pay a monthly mortgage bill, the payment amount remains identical each month (assuming a fixed-rate loan). However, the internal distribution of that payment changes constantly. In the banking world, this mathematical progression is known as amortization.

Understanding how this process functions is crucial for building long-term wealth through real estate. Knowing how the division of interest and principal changes over the term helps you make informed choices regarding loan prepayments and payoff structures.

The Front-Loaded Interest Phenomenon

Many new homeowners are shocked to discover that after making payments for several years, their outstanding loan balance has barely decreased. This is not an error; it is the natural mathematical result of how amortization schedules are structured.

Because interest is calculated as a percentage of the remaining loan balance, and the loan balance is at its highest at the start of the term, the interest fee is also at its peak. In a typical 30-year mortgage at 6.5% interest, over 70% of your very first monthly payment goes toward interest charges, leaving less than 30% to reduce the principal balance. As you slowly pay down the principal, the outstanding balance decreases, which in turn reduces the monthly interest fee. More of your monthly payment is then directed toward principal reduction, accelerating your equity growth.

Analyzing the Amortization Curve

The shift from paying mostly interest to mostly principal is not linear. It follows an exponential curve:

- Years 1 to 10: The interest phase. The majority of your monthly cash flow is directed to interest fees. Your equity accumulation is slow.

- Years 11 to 20: The balance shift. The principal portion of the payment rises steadily, eventually matching the interest portion around year 15 to 18.

- Years 21 to 30: The acceleration phase. With the loan balance significantly reduced, interest fees drop, and almost the entire monthly payment goes directly toward paying off the remaining principal.

This curve demonstrates why choosing a 15-year term is so impactful. By shortening the term, you skip the high-interest initial years of a 30-year curve, starting at a much steeper point on the equity accumulation curve.

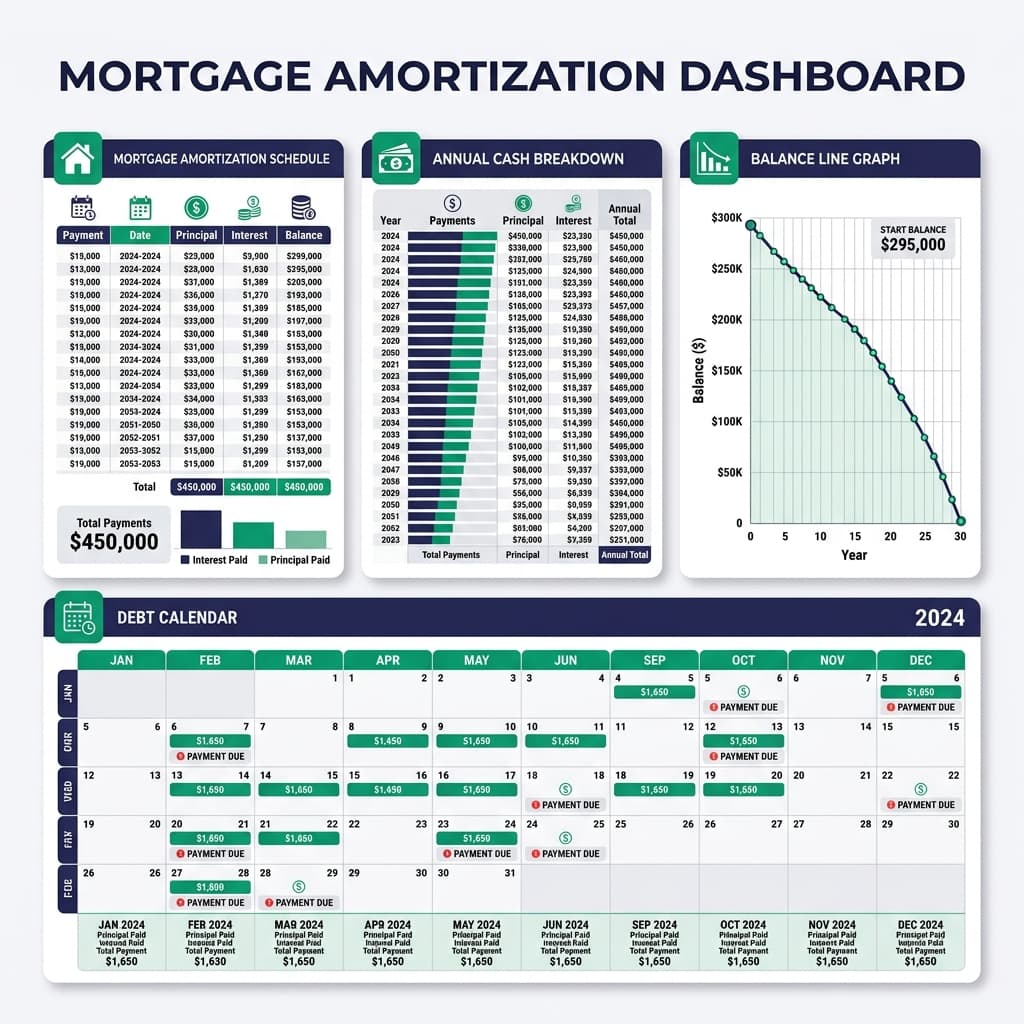

How to Read an Amortization Table

An amortization table provides a year-by-year breakdown of your loan's progress. Here is what each column represents:

- Year/Payment Number: Tracks your progress through the loan term.

- Principal Paid: The total amount of money you have paid directly toward reducing your loan balance during that year.

- Interest Paid: The total amount of money paid to the lender during the year as financing charges.

- Remaining Balance: The outstanding balance you still owe the lender at the end of that year.

The Amortization Calculation Formula

The fixed monthly principal and interest payment (M) on an amortizing loan is calculated using the standard amortization equation, which factors in your principal loan size (P), monthly interest rate (r), and total number of payments (n):

P = Principal loan amount

n= Total payment periods (Years × 12)

Each month, the interest fee is calculated first as P × r, which is paid to the lender. The remaining portion of your monthly payment (M - Interest) is then applied to reduce your principal balance (P), setting the new balance for the following month's interest calculation.

Amortization in Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

An amortization schedule works differently depending on the type of loan you choose. For a fixed-rate mortgage, the schedule is set in stone from day one; your monthly principal and interest payment remains constant, and the transition from interest to principal follows a predictable path.

For an adjustable-rate mortgage (ARM), the schedule is periodically recalculated. During the initial fixed period (e.g., the first 5 or 7 years of a 5/1 or 7/1 ARM), payments amortize exactly like a fixed-rate loan. However, once the interest rate adjusts based on market indexes, your monthly payment is recalculated ("re-amortized") over the remaining years of the term to ensure the loan is still paid off on time. This can cause sudden, significant changes in your monthly payment and shift the equity accumulation timeline.

The Compounding Power of Extra Payments

Because amortization interest is calculated monthly based on your outstanding balance, reducing that balance early yields massive long-term savings.

Any extra payment you make goes directly toward reducing the principal balance, bypassing the interest fee entirely. This permanently lowers your outstanding balance, which reduces the interest charges for every single remaining month of the loan. This creates a powerful compounding effect, shortening your loan term and saving thousands of dollars in interest costs over time.

Amortization Schedule FAQ

An amortization schedule is a complete table showing each periodic payment on an amortizing loan. It details the portion of each payment that goes toward interest versus principal, and tracks the declining outstanding balance of the loan until it is paid off at the end of the term.

Interest is calculated as a percentage of your remaining unpaid principal balance. Since your loan balance is highest at the beginning of your term, the interest portion of your monthly payment is also at its peak. As you pay down the principal over time, subsequent interest charges decrease, allowing more of your payment to go toward principal.

Any extra payment applied directly to your principal reduces the outstanding balance immediately. Because future monthly interest is calculated on a lower balance, your future monthly interest charges decrease. This means more of your regular payments go toward principal, accelerating your equity growth and shortening the overall term.

Yes. When you refinance into a new loan (for example, a new 30-year fixed-rate mortgage), the amortization schedule resets back to year one. Even if your interest rate is lower, this reset means you start back at the high-interest phase, which can increase the total lifetime interest paid unless you choose a shorter term (such as a 15-year or 20-year refinance).

A 15-year mortgage has higher monthly payments, but it amortizes much faster. You build equity at a much steeper rate, pay off the loan in half the time, and usually qualify for a lower interest rate, which saves you tens or even hundreds of thousands of dollars in lifetime interest charges compared to a 30-year loan.