Buying a home with student loans is fully possible because lenders focus entirely on your monthly debt payment rather than your overall principal balance. Conventional loans accept a documented $0 Income-Driven Repayment (IDR) monthly payment. FHA loans require using 0.5% of your total student loan balance as a monthly payment placeholder if your payment is zero or deferred. Homebuyers can determine how these payment variables affect their qualifying limit using a home affordability calculator.

Carrying student loan debt is one of the most common concerns for prospective homebuyers. It is easy to assume that a large student loan balance will disqualify you from getting a mortgage. Fortunately, mortgage underwriting rules do not compare your total outstanding loan balance to your income. Instead, they look at your recurring monthly debt commitments.

Lenders measure your monthly commitments using a debt-to-income (DTI) ratio. To see how these calculations define your budget, check our guide on how the 28/36 rule works, or run your numbers through our interactive home affordability calculator.

How Student Loans Impact Your DTI Ratio

Your DTI ratio is the percentage of your gross monthly income that goes toward paying recurring debts. The back-end DTI includes your proposed mortgage payment, property taxes, homeowners insurance, credit cards, auto loans, and your student loans.

Because a student loan payment is a recurring debt, it directly occupies a portion of your allowable DTI window. If your gross monthly income is $8,000, a lender operating under a conservative 36% DTI limit allows a total monthly debt cap of $2,880. If you have a monthly student loan payment of $400, your remaining allowance for your mortgage PITI payment drops from $2,880 to $2,480.

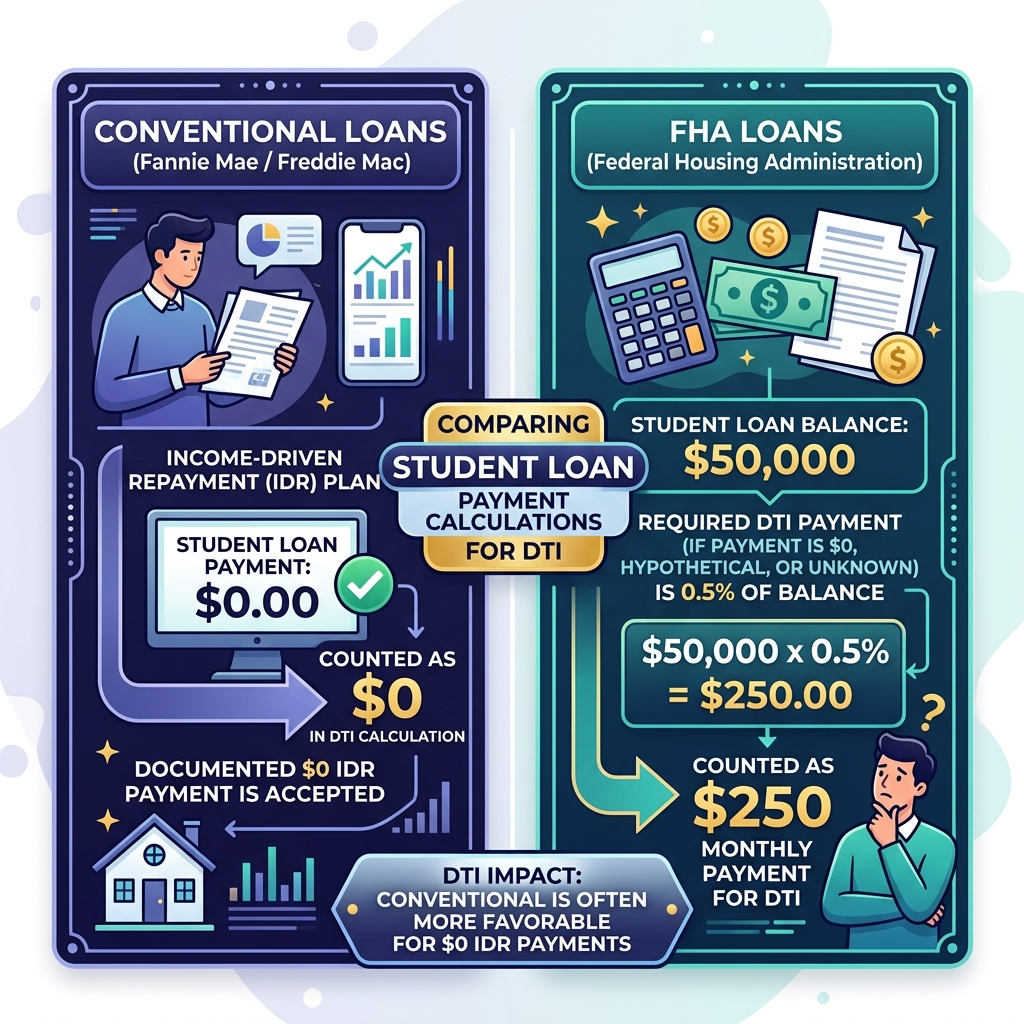

Figure 1: How conventional loans allow actual $0 IDR payments compared to FHA loans requiring a 0.5% balance calculation for DTI qualifying.

Underwriting Guidelines: FHA vs. Conventional Loans

The way lenders treat your student loans depends heavily on the type of mortgage you apply for. Understanding these rules is essential if your student loans are currently on an Income-Driven Repayment (IDR) plan or in deferment.

Conventional Loans (Fannie Mae & Freddie Mac)

Conventional guidelines are highly favorable for borrowers on IDR plans. According to rules set by the housing finance enterprise Fannie Mae, if your monthly student loan payment is documented as $0 on your credit report, the lender can use $0 in your DTI calculation.

If your loans are in deferment or forbearance, conventional lenders will require you to provide documentation showing what your payment will be when the deferment ends. If you cannot provide this, the lender must calculate a monthly payment equal to 1% of your total loan balance.

FHA Loans (Federal Housing Administration)

FHA guidelines do not permit a $0 payment in DTI calculations. Under FHA rules, if your monthly payment on an IDR plan is $0, or if your loans are deferred, the lender is required to calculate a monthly payment equal to 0.5% of your total student loan balance.

For example, if you have a total student loan balance of $60,000, FHA rules require the underwriter to insert a monthly payment of $300 into your debt profile, regardless of whether your actual payment is $0. This can reduce your home purchase budget significantly.

Case Study: DTI Calculation Comparison

Let us compare how Conventional vs FHA guidelines calculate student loans in DTI math. Consider a buyer with a $60,000 student loan balance on an IDR plan with a $0 payment, earning a gross monthly income of $8,000:

| Mortgage Type | Underwriting Rule | Counted Monthly Debt | Remaining DTI Space |

|---|---|---|---|

| Conventional Loan | Accepts IDR $0 Payment | $0 / month | 100% of DTI allowance |

| FHA Loan | Requires 0.5% of Balance | $300 / month | DTI allowance reduced by $300 |

In this scenario, choosing a conventional loan frees up an additional $300 of monthly purchasing power, making it easier to qualify for a higher purchase budget.

Strategies to Maximize Your Homebuying Power

If you have student loans and want to qualify for a mortgage, there are several steps you can take to optimize your profile before applying:

- Get a Documented IDR Plan: If you are applying for a conventional loan, make sure your $0 or reduced payment is formally documented. You can review and apply for plans on the federal **[U.S. Department of Education Student Aid](https://studentaid.gov)** website.

- Pay Off Small Debts: Paying off credit card balances or car loans will lower your total monthly debt, offseting the impact of your student loans.

- Refinance Student Loans: If your monthly payments are high and you do not plan to use government forgiveness programs, refinancing your student loans to secure a lower payment can improve your mortgage qualifying limits.

The Bottom Line

Student loan debt does not prevent you from buying a home. By selecting the correct mortgage program and utilizing strategic repayment structures, you can find a loan that accommodates your financial profile and lets you move forward on homeownership.

Analyze Your Debt-to-Income Limits

Plug your monthly student loans and gross income into our affordability calculator to model conventional vs FHA DTI caps.