The 28/36 rule is a financial guideline that lenders use to calculate your home buying budget based on your debt-to-income (DTI) ratio. Under this rule, no more than 28% of your gross monthly income should go toward housing costs (Principal, Interest, Taxes, and Insurance), and no more than 36% should cover total debt payments (housing costs plus recurring debts like auto loans, student loans, and credit cards). Lenders use these percentages as safety thresholds; staying within them maximizes your borrowing power and protects you from becoming house poor.

When you apply for a mortgage, underwriters do not guess how much you can borrow. They use math to measure your ability to make payments. The primary formula they use is the 28/36 rule.

To estimate your DTI limits, check our home affordability calculator. Let us break down how these two limits define your maximum home purchase.

The Front-End Limit: 28% for Housing Costs

The first number represents the front-end ratio, which governs your direct housing costs. According to guidelines, your total monthly housing cost—which includes Principal, Interest, Taxes, and Insurance (PITI)—should not exceed 28% of your gross monthly income.

For example, if your gross household income is $10,000 per month, your maximum housing payment should be:$10,000 x 0.28 = $2,800

This $2,800 must cover your total mortgage payment. If your down payment is less than 20%, it must also cover your Private Mortgage Insurance (PMI) premiums. You can calculate these monthly components using our mortgage payment calculator.

The Back-End Limit: 36% for Total Debt

The second number represents the back-end ratio. This limit looks at your complete monthly debt profile. It states that your housing cost plus all other recurring monthly debts should not exceed 36% of your gross monthly income.

Recurring monthly debts include:

- Minimum credit card payments.

- Student loan payments.

- Car loans.

- Personal loans or child support.

If your gross monthly income is $10,000, your total debt ceiling is:$10,000 x 0.36 = $3,600

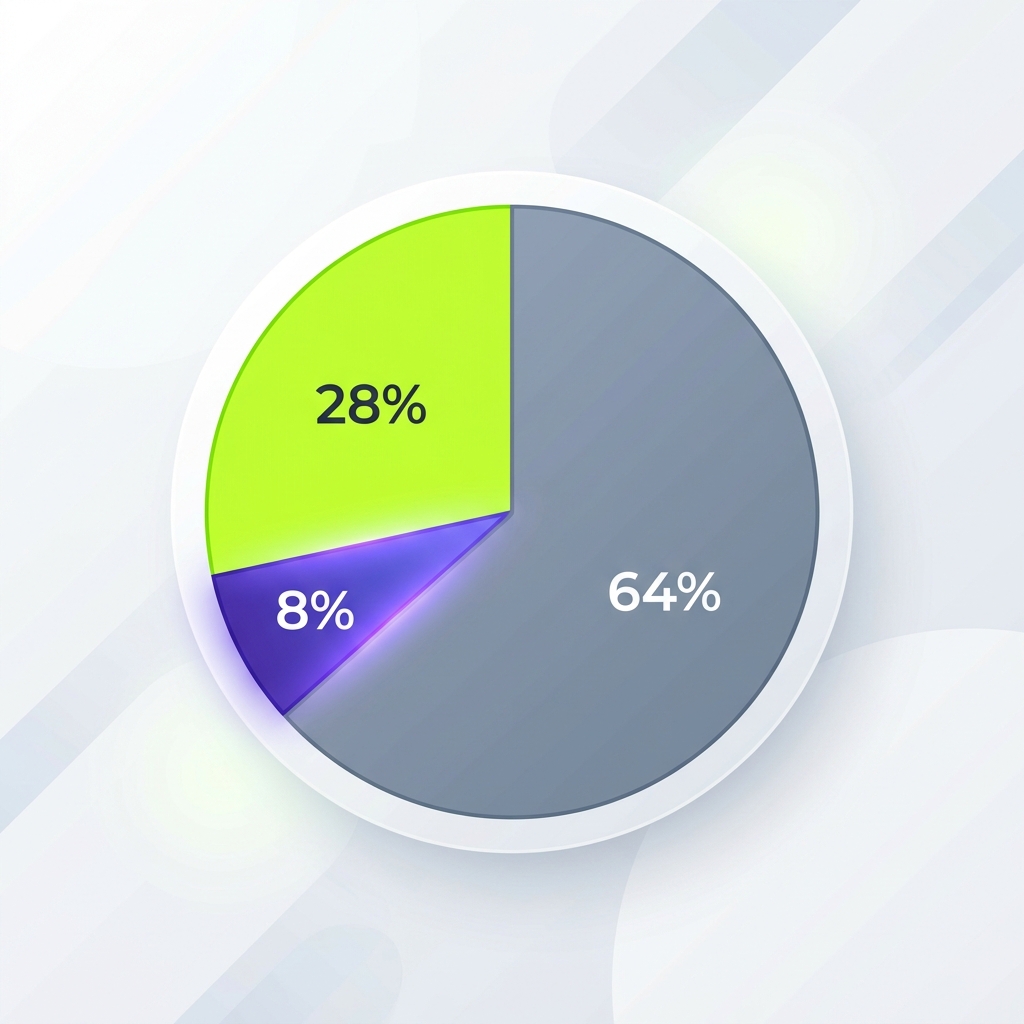

Figure 1: How gross income is divided under the 28/36 rule, allocating 28% to housing and 8% to other debt, leaving 64% for taxes and living costs.

How Lenders Determine Your Actual Budget Limit

Lenders calculate both the 28% limit and the 36% limit. They then qualify you based on the lower of the two numbers. This is a crucial detail that catches many first time buyers off guard.

Let us look at two scenarios with a gross income of $10,000 per month:

Scenario A: Low Debt (Only a $200 car payment)

- Under the 28% front-end limit, you qualify for a $2,800 payment.

- Under the 36% back-end limit, your total debt cap is $3,600. Subtracting the $200 car payment leaves a $3,400 housing payment.

- Outcome: Lenders qualify you based on the lower of the two limits: $2,800. Your low debt allows you to utilize the full 28% housing ratio.

Scenario B: High Debt ($600 car payment + $400 student loans)

- Under the 28% front-end limit, you qualify for a $2,800 payment.

- Under the 36% back-end limit, your total debt cap is $3,600. Subtracting the $1,000 debt leaves a $2,600 housing payment.

- Outcome: Lenders qualify you based on the lower of the two limits: $2,600. Your recurring debt drags down your housing budget.

This comparison shows why paying off auto loans or student debt before applying for a mortgage directly increases the size of the house you can buy. Reviewing your payoff strategies on our amortization schedule page is a great way to plan your debt paydown.

How Credit Guidelines View the 28/36 Rule

The 28/36 rule is the benchmark for conventional mortgages backed by GSEs like Fannie Mae. According to the Consumer Financial Protection Bureau, a back-end DTI ratio of 36% or less is typical for a Qualified Mortgage (QM), although some government programs like FHA loans allow higher ratios.

The Bottom Line

Understanding the 28/36 rule helps you see your finances through a lender's eyes. Before shopping for homes, use these ratios to evaluate your income. Keeping your payments within these limits ensures you have a secure budget for years to come.

Calculate Your Debt-to-Income Limits

Connect these ratio thresholds to your actual income and monthly debts. Use our home affordability tool to see your limits.