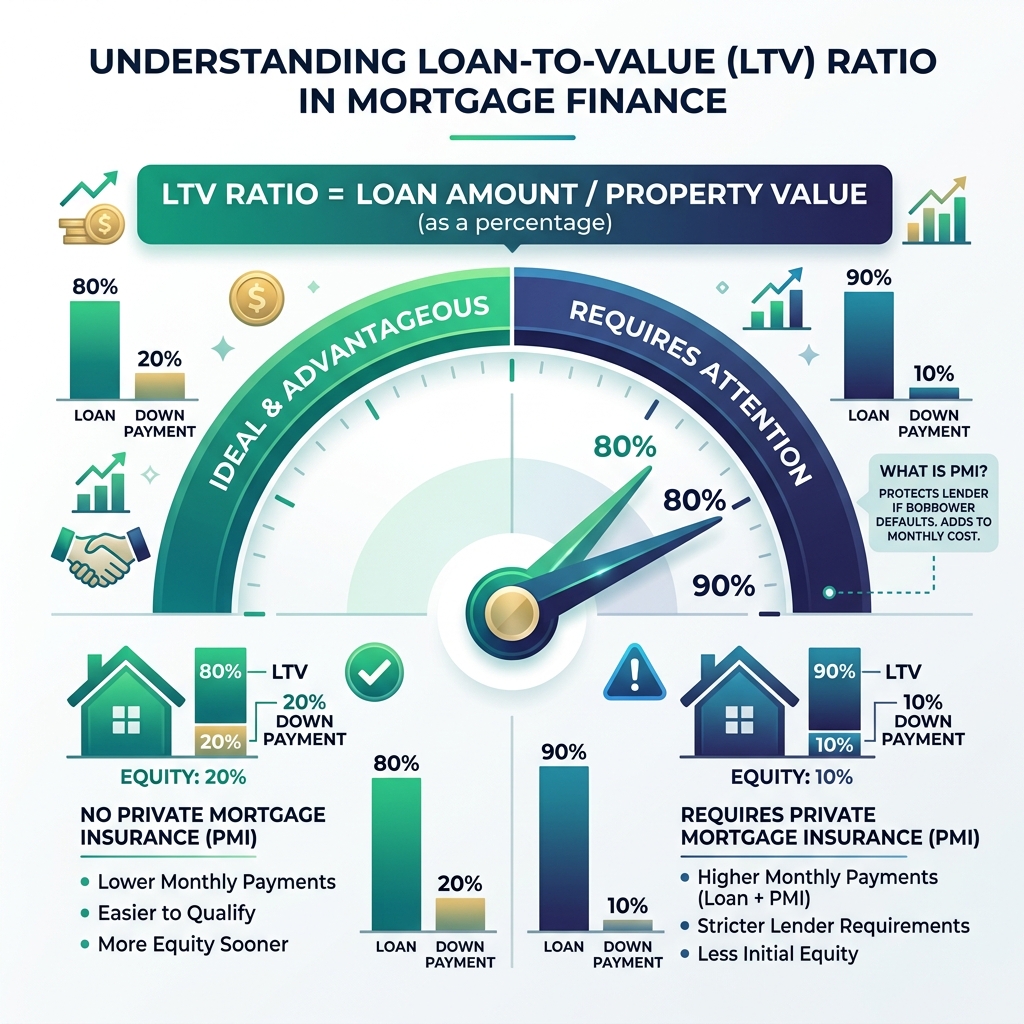

Private Mortgage Insurance (PMI) is a monthly fee required by conventional lenders when a home buyer puts down less than 20%. PMI does not protect the buyer. Instead, it protects the lender if the buyer defaults on the mortgage. PMI typically costs between 0.2% and 2.0% of the loan amount annually. Buyers can avoid PMI by putting down a full 20%, or cancel it once they reach 20% equity through home price growth or principal paydowns.

Saving enough cash for a home down payment is one of the biggest challenges for modern home buyers. While many mortgage options allow down payments as low as 3% or 5%, these low down payment options come with a hidden monthly cost: Private Mortgage Insurance. If you want to accelerate your savings rate, you can utilize key strategies to build your home down payment fund faster.

PMI is a premium added to your monthly mortgage bill, becoming a standard part of your total monthly mortgage payment (PITI). It protects the financial institution in case you stop making your payments, meaning you pay the premiums but receive none of the direct benefits. To see how adding a monthly premium changes your total housing costs, you can run calculations on our main monthly mortgage calculator or evaluate your target purchase limits using our home affordability calculator.

How Private Mortgage Insurance Works

When you purchase a home with a conventional loan, lenders evaluate your risk using the Loan-to-Value (LTV) ratio. The LTV ratio measures the size of your mortgage against the value of the property. If your LTV ratio is above 80%, meaning you put down less than 20% of the purchase price, the lender will require PMI. To review your legal rights regarding cancellation, you can consult the guidelines hosted by the Consumer Financial Protection Bureau (CFPB) under the Homeowners Protection Act, or check conventional loan parameters outlined by Fannie Mae.

Four Strategies to Avoid or Cancel PMI

You do not have to pay PMI forever. There are several ways to avoid this monthly fee from the start or cancel it early once you build up equity in your home:

Make a 20% Down Payment

The simplest way to avoid PMI is by putting down 20% or more of the home's purchase price at closing. By keeping your LTV ratio at or below 80%, conventional lenders will automatically waive the PMI requirement, instantly lowering your monthly payments.

Request Automatic or Manual Cancellation at 80% LTV

Under federal law, conventional lenders must automatically cancel PMI once your loan balance is scheduled to reach 78% of the original home value. However, you can write to request cancellation as soon as your balance drops to 80% LTV. Keep close track of your loan balance to request this early.

Get a New Home Appraisal After Values Rise

If home values rise in your neighborhood or you complete major home improvements, your equity may climb to 20% ahead of schedule. You can contact your lender and request a new official home appraisal. If the appraisal shows your loan balance is under 80% of the new value, you can request PMI removal.

Consider Lender-Paid Mortgage Insurance (LPMI)

With LPMI, the lender pays your mortgage insurance premium upfront in exchange for a slightly higher interest rate on your loan. This can be beneficial if you plan to stay in the home for a short time. However, unlike standard PMI, this higher rate remains for the entire life of the mortgage.

Figure 1: The transition zone below the 80% LTV threshold allows conventional borrowers to eliminate monthly PMI premiums.

The Long-Term Impact of Eliminating PMI

Removing PMI lowers your monthly housing payment, which instantly frees up cash in your family budget. You can redirect these savings toward principal prepayments, investments, or home maintenance costs.

Review Your True Monthly PITI Payments

Connect your purchase details and check how different down payment percentages change your LTV ratio and monthly PMI insurance costs.