Saving for a down payment does not have to take a decade. By optimizing your cash storage in high-yield accounts, automating your monthly savings goals, and tapping into government assistance programs, you can reach your milestone much sooner. Visualizing how down payments shape your monthly budget makes it easier to set target saving limits.

The biggest hurdle to owning a home is almost always saving the down payment. With home prices rising, putting together enough cash can feel like trying to hit a moving target.

Fortunately, you do not necessarily need a 20% down payment to purchase a home. Lenders offer several low down payment options. To see how your upfront cash affects your loan limits and monthly costs, check out our interactive home affordability calculator.

To better understand what your monthly expenses will look like once you buy, you can read our guide on understanding mortgage PITI components. You can also explore how underwriters look at your recurring debts in our analysis of how the 28/36 rule works.

7 Actionable Down Payment Saving Strategies

Here are seven practical, real-world methods to build your down payment fund quickly:

Switch to a High-Yield Savings Account (HYSA)

Keeping your down payment cash in a brick-and-mortar bank savings account means earning a negligible interest rate, often as low as 0.01%. Shifting your money to an online high-yield savings account (HYSA) can boost your earnings to 4% or 5% annually. On a $40,000 balance, that difference yields an extra $2,000 in interest per year, completely risk-free and liquid.

Automate the "Pay Yourself First" Strategy

Rather than saving whatever money is left at the end of the month, set up an automatic transfer from your paycheck directly into your down payment account on paydays. If the money is moved before you have a chance to spend it, you adjust your lifestyle to fit the remaining balance, ensuring consistent monthly progress.

Leverage Family Gift Funds

Many loan programs allow buyers to use cash gifts from family members to cover all or part of the down payment. Lenders require a formal gift letter signed by the donor, stating that the funds are a gift and do not need to be repaid. This is a common way first-time buyers cross the finish line.

Tap Into Down Payment Assistance (DPA) Programs

Thousands of DPA programs are available through local and state housing authorities. These programs provide grants or zero-interest loans that help buyers cover their down payments. You can check programs in your area through the U.S. Department of Housing and Urban Development (HUD) website.

Utilize First-Time Buyer Retirement Exemptions

The IRS allows first-time buyers to withdraw up to $10,000 from an IRA without the standard 10% early withdrawal penalty. Additionally, you can explore borrowing from your employer-sponsored 401(k) plan. While you must pay back a 401(k) loan with interest, that interest is paid directly back into your own retirement account.

Dedicate Side Income Exclusively to Savings

If you have a side hustle, freelance business, or receive annual work bonuses, allocate 100% of those non-standard funds straight to your down payment account. Since this income is separate from your primary salary used to cover your baseline living expenses, it acts as pure accelerant for your savings goal.

Perform a Recurring Expense Audit

Audit your credit card statements from the last three months and eliminate recurring subscriptions, memberships, and unused services. Redirecting even $150 a month in minor subscription cancellations translates to an extra $1,800 saved over the year.

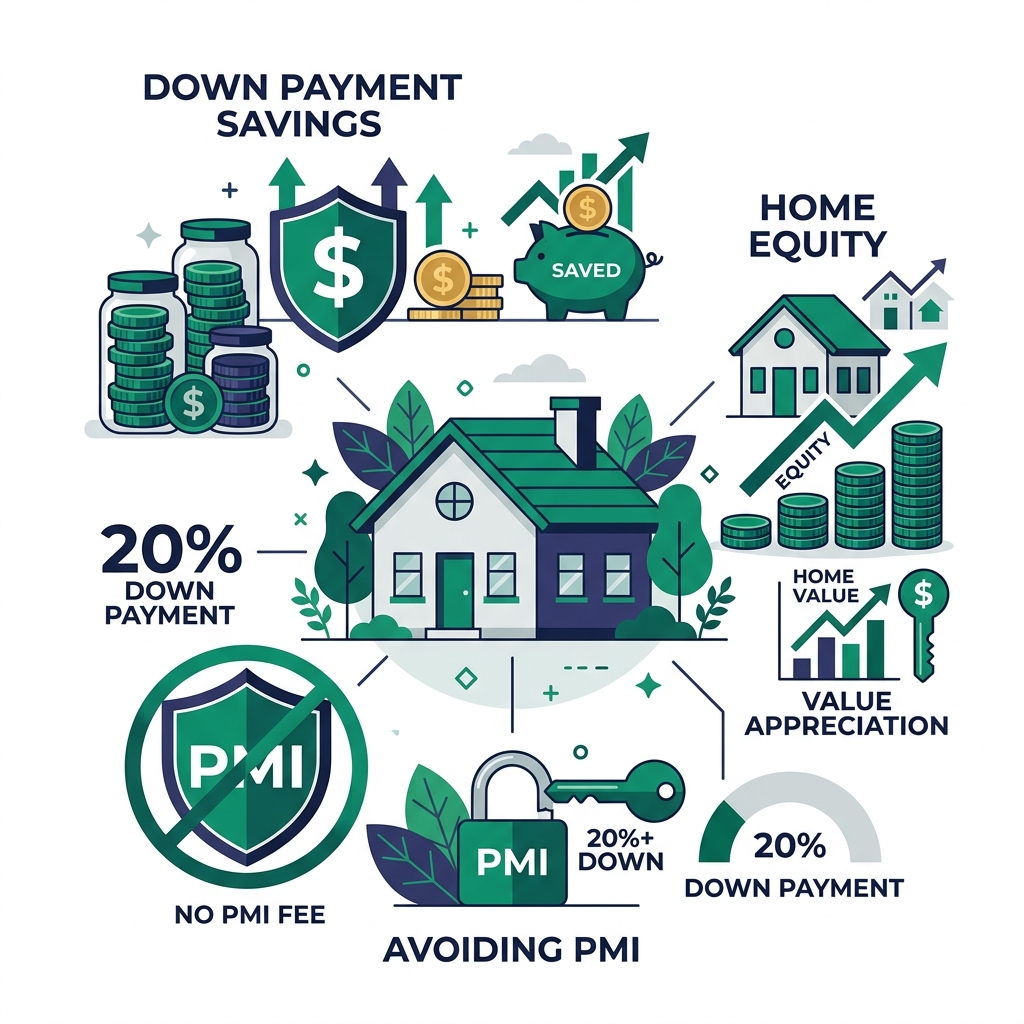

Figure 1: Accumulating home equity starts with building a robust down payment fund to unlock favorable borrowing parameters.

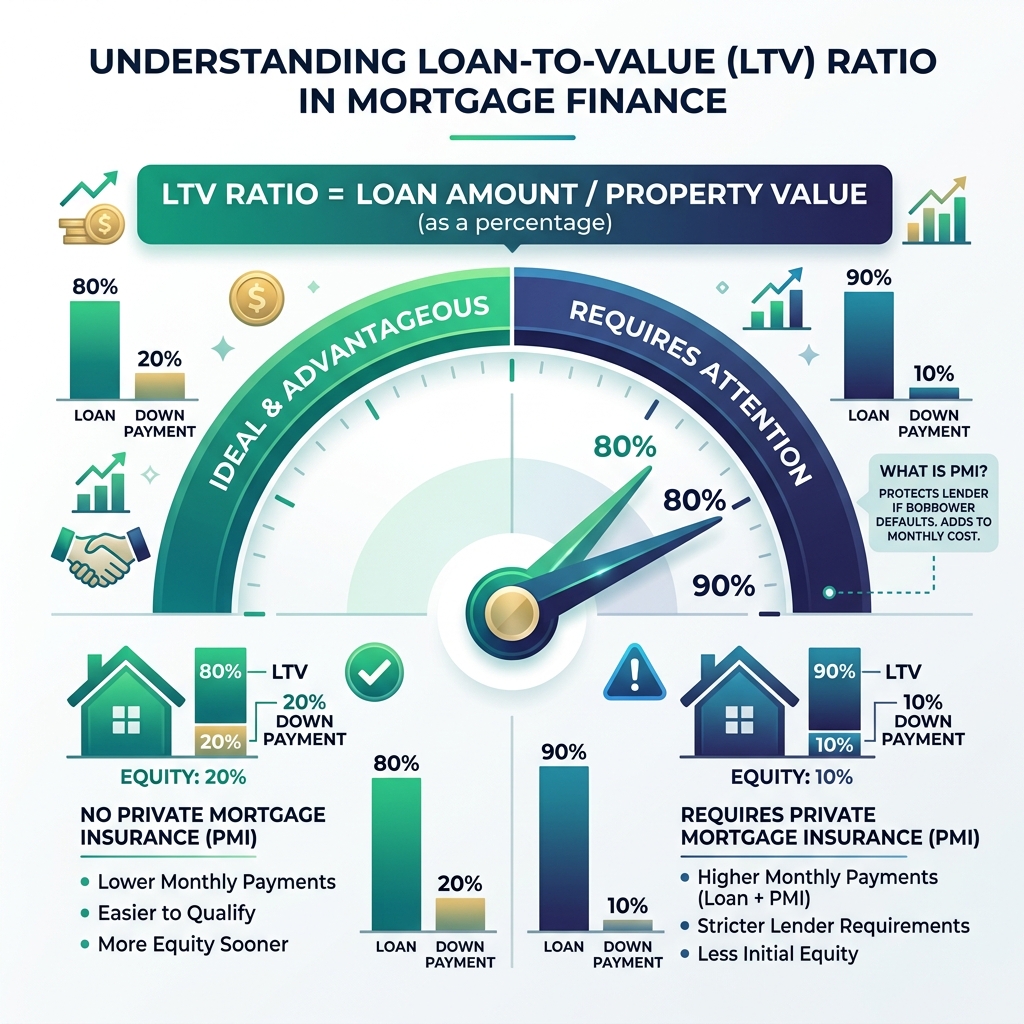

The Long-Term Value of a Higher Down Payment

While low down payment programs are excellent for getting into a home sooner, putting more money down upfront has massive long-term benefits.

By putting 20% down, you completely avoid private mortgage insurance (PMI) fees, which typically cost 0.5% to 1.5% of the loan amount annually. A higher down payment also lowers your total loan balance, which dramatically cuts the interest you will pay over the life of the mortgage.

You can verify standard home purchase guidelines and find more educational home buying resources on the Consumer Financial Protection Bureau (CFPB) website.

Calculate Your Home Purchasing Budget

Connect your current savings balance and target monthly payment into our calculator to map out your maximum home price and down payment ratios.