PITI stands for Principal, Interest, Taxes, and Insurance. These are the 4 parts of your monthly mortgage payment: Principal (the portion that pays down your outstanding loan balance), Interest (the lender's fee for borrowing the capital), Taxes (monthly escrow for local property levies), and Insurance (homeowners protection premiums). Understanding how these elements work together is essential to calculating your total housing cost and determining how much house you can actually afford.

When you purchase a home, the sticker price is only one part of the financial equation. Lenders calculate your loan qualification using your monthly housing obligation. This total amount is split into four distinct financial boxes.

Lenders refer to this monthly total as PITI. If you are using our mortgage payment calculator, you will notice these factors are automatically calculated. Let us examine each component.

PPrincipal: The Loan Balance Paydown

The principal is the money that goes directly toward reducing the balance of your loan. For example, if you borrow $300,000 to buy a property, the principal portion of your payment chips away at that $300,000 debt. In the early stages of a loan, only a small fraction of your check goes toward the principal. Over time, that portion increases. You can visualize this trajectory using our amortization schedule page.

IInterest: The Borrowing Fee

Interest is the fee you pay to the lender for borrowing their capital. It is determined by your loan’s interest rate and outstanding balance. In the first few years of your mortgage, interest accounts for the largest share of your monthly payment. Reducing this cost over time is a primary goal for many homeowners, and making extra payments directly toward the principal balance can help save thousands in interest fees.

TTaxes: Property Assessments

Local governments levy property taxes to fund public services, including schools, roads, and emergency departments. Lenders divide your annual property tax bill by 12 and include it in your monthly payment. This money is held in an escrow account, and your loan servicer pays the local tax authority when the bill comes due. Tax rates vary by state, county, and school district.

IInsurance: Protecting Your Investment

This component includes homeowners insurance, which protects your home and personal belongings against fires, storms, and theft. Like property taxes, homeowners insurance is typically collected monthly into your escrow account and paid out annually by your servicer. If your home is in a high-risk flood plain or earthquake zone, you may need additional specialized insurance policies.

Figure 1: How the four PITI elements stack together to build your total monthly mortgage obligation.

How Lenders Use PITI to Evaluate Your Income

Underwriting guidelines, such as those set by Fannie Mae, rely heavily on your PITI calculation. Lenders look at two key metrics:

1. Front-End DTI Ratio: Your total monthly housing payment (PITI) divided by your gross monthly income. Lenders prefer this ratio to remain under 28%.

2. Back-End DTI Ratio: Your housing payment plus all other monthly recurring debt obligations (such as car payments, student loans, and credit cards) divided by gross income. Lenders prefer this ratio to remain under 36%.

If you want to determine your borrowing limits using these ratios, you can try our home affordability calculator.

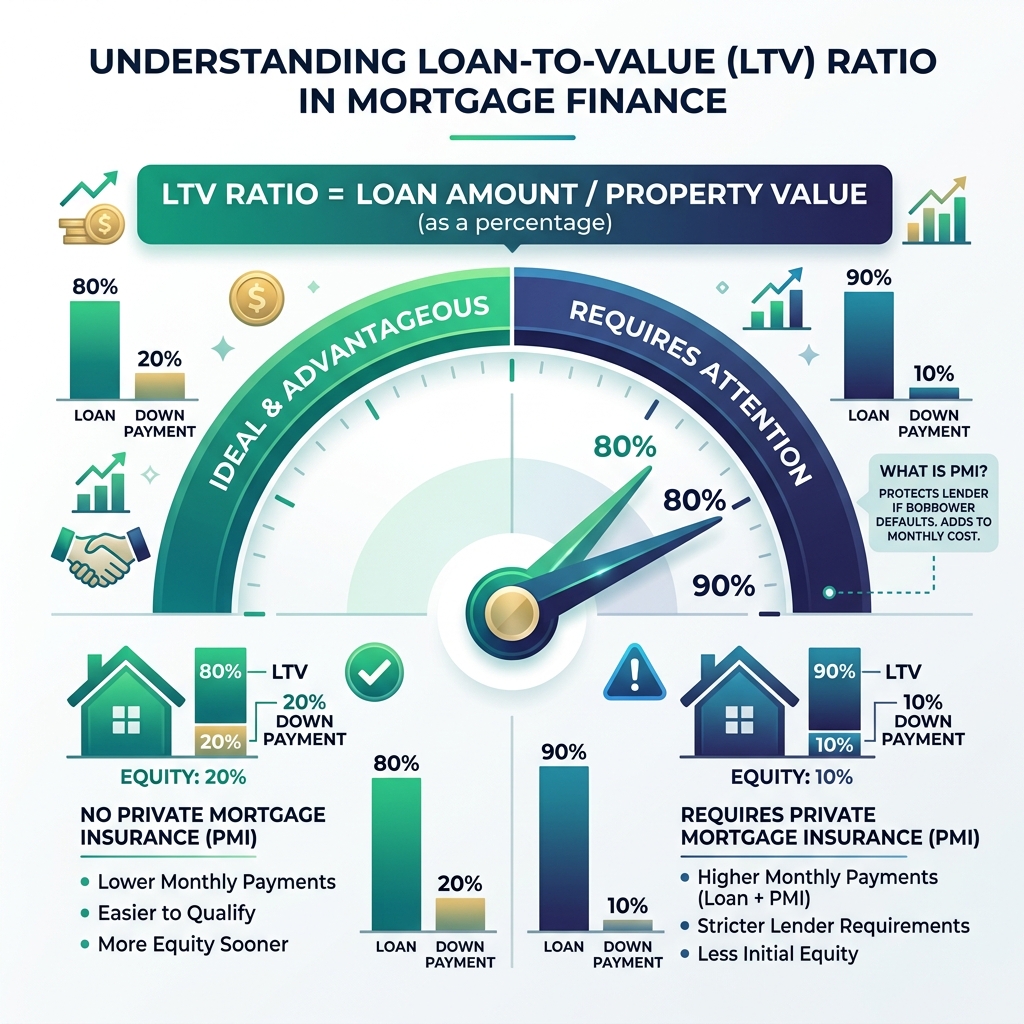

The "Fifth" Component: Private Mortgage Insurance (PMI)

If your down payment is less than 20% on a conventional loan, your monthly payment will include an extra fee. The Consumer Financial Protection Bureau defines this as Private Mortgage Insurance (PMI). Lenders collect this premium to protect themselves in case of borrower default, and it is usually bundled directly into the insurance (I) portion of your PITI payment.

The Bottom Line

Mastering PITI enables you to look past the listing price of a home and assess the true monthly cost. Knowing how tax rates, home insurance, and interest rates influence your check keeps you in control of your household budget.

Calculate Your True PITI Payment Now

Ready to plug in your numbers? Use our primary payment tool to adjust interest rates, estimate property taxes, and calculate your total monthly check.