Owning a home incurs substantial expenses beyond the monthly mortgage payment, including maintenance, rising property taxes, HOA fees, insurance adjustments, and private mortgage insurance. Standard maintenance averages 1% to 2% of the home's value annually. Property taxes and insurance premiums fluctuate year-over-year, which can trigger significant increases in your escrow payment. Homebuyers must factor these ongoing financial obligations into their budget using a home affordability calculator to avoid buying more house than they can realistically afford.

Most first-time homebuyers focus entirely on saving for a down payment and securing a monthly mortgage payment that fits their current budget. This narrow focus can lead to financial strain shortly after moving in. Owning a home comes with a list of ongoing transactional, municipal, and maintenance expenses that do not exist in a rental setup.

Before signing a contract, comparing the lifestyle costs of buying versus renting using a rent vs buy analysis is a great step. To budget for these variables, you can calculate conservative parameters using our home affordability calculator. Here are the five hidden costs of homeownership you must prepare for.

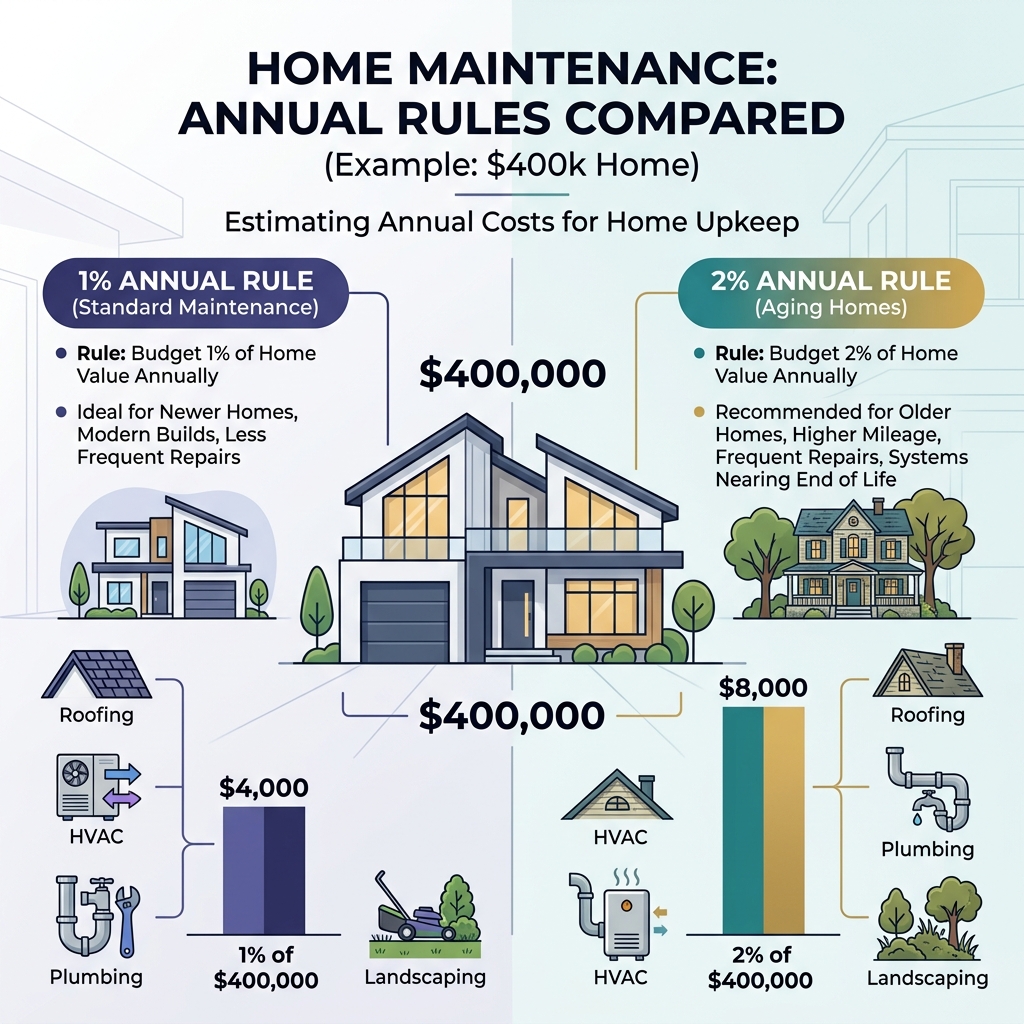

Home Maintenance and Repairs (The 1% to 2% Rule)

When you rent, a leaky pipe or broken air conditioner is your landlord's financial problem. When you buy, you are the landlord. Roofs wear out, water heaters leak, and HVAC systems fail. These repairs must be paid out of pocket immediately.

The standard guideline is to budget 1% to 2% of your home's value annually for upkeep. For a home valued at $400,000, this equates to $4,000 to $8,000 per year, or roughly $330 to $660 monthly, put aside in a dedicated repair fund. To find resources and tips for managing home maintenance, the U.S. government offers guidelines on the Department of Housing and Urban Development (HUD) website.

Figure 1: Comparison between standard home maintenance rules, illustrating the difference in annual savings required for newer homes versus older properties.

Property Tax Reassessments and Supplemental Bills

Property taxes are rarely stable. When you buy a home, the transaction triggers a reassessment by the county tax assessor. If the previous owner bought the house twenty years ago, they paid taxes on an outdated valuation. Shortly after closing, you will likely receive a reassessed tax bill based on your purchase price, accompanied by a one-time supplemental tax bill to cover the difference for the current year.

These updates can significantly alter your monthly payments. To understand how taxes are bundled, read our guide on understanding mortgage PITI payments. For information on property tax deductions and federal guidelines, you can review current tax codes on the official Internal Revenue Service (IRS) portal.

Homeowners Association (HOA) Dues and Special Assessments

If you purchase a property within a planned subdivision, townhouse community, or condominium building, you will likely pay mandatory homeowners association (HOA) fees. These fees pay for shared maintenance, trash pickup, landscaping, and community amenities.

Monthly HOA dues are not fixed. Boards can vote to increase dues to keep pace with operational inflation. In addition, if major shared infrastructure fails, such as a parking garage roof or building facade, and the association's reserve fund is insufficient, the board can levy a mandatory Special Assessment. This requires every homeowner to pay a sudden, lump-sum bill of thousands of dollars to cover the project.

Volatile Homeowners Insurance Premiums

Homeowners insurance is required by all mortgage lenders. While you might secure an affordable premium rate at closing, these rates frequently rise. Extreme weather events and soaring material replacement costs have driven insurance premiums upward nationwide.

If your property is in an area prone to floods, wildfires, or hurricanes, standard insurance policies will not cover these events. You will need to purchase separate specialty policies, which can add hundreds of dollars to your monthly housing expenses. To compare state-by-state insurance trends and regulations, you can check consumer alerts on the National Association of Insurance Commissioners (NAIC) site.

Private Mortgage Insurance (PMI)

If you borrow conventional loan funds and put down less than 20% at purchase, lenders will charge you Private Mortgage Insurance (PMI). This premium typically costs 0.5% to 1.5% of the total loan amount annually and is divided into your monthly mortgage payment.

PMI offers no protection for you. It strictly protects the lender if you default and foreclosure occurs. This monthly fee is a direct addition to your housing cost until you build 20% equity in the property, at which point you can request to cancel the coverage.

The Bottom Line

Homeownership is a highly rewarding path to building long-term wealth, but it requires thorough financial planning. Setting aside liquid emergency cash for repairs, reviewing tax assessment histories, and keeping a conservative budget buffer are the keys to ensuring that the hidden costs of owning a home do not derail your financial progress.

Test Your True Purchasing Power

Use our calculator to estimate your monthly PITI ratios, simulate down payment variations, and verify how tax adjustments shape your bottom line.