Lowering closing costs is key to preserving cash when buying a home. Lender credits reduce upfront costs by increasing the interest rate, which increases monthly payments. Seller concessions involve the seller paying a portion of the closing fees, leaving the interest rate unaffected. Combining both can bring cash requirements to a minimum, and calculating these tradeoffs is easier when visualizing long-term costs.

Buying a home requires a significant amount of cash. Most buyers spend months, or even years, saving for a down payment. However, many are surprised by the additional thousands of dollars needed for closing costs. These fees usually range from 2% to 5% of the total loan amount, covering everything from lender origination fees to title insurance.

If you want to keep more money in your bank account, you have two primary options: lender credits and seller concessions. While both options reduce your out-of-pocket costs at closing, they function in completely different ways and have distinct financial impacts.

To see how closing fees fit into the larger picture of purchasing or refinancing, check out our guide on the true cost of refinancing and closing costs. You can also explore how escrow accounts impact these upfront charges in our detailed look at how mortgage escrow accounts work.

Understanding Lender Credits

Lender credits are essentially an agreement where your mortgage provider pays a portion of your closing costs. In return, you agree to pay a slightly higher interest rate on your loan. This is often referred to as a premium rate.

How Lender Credits Work

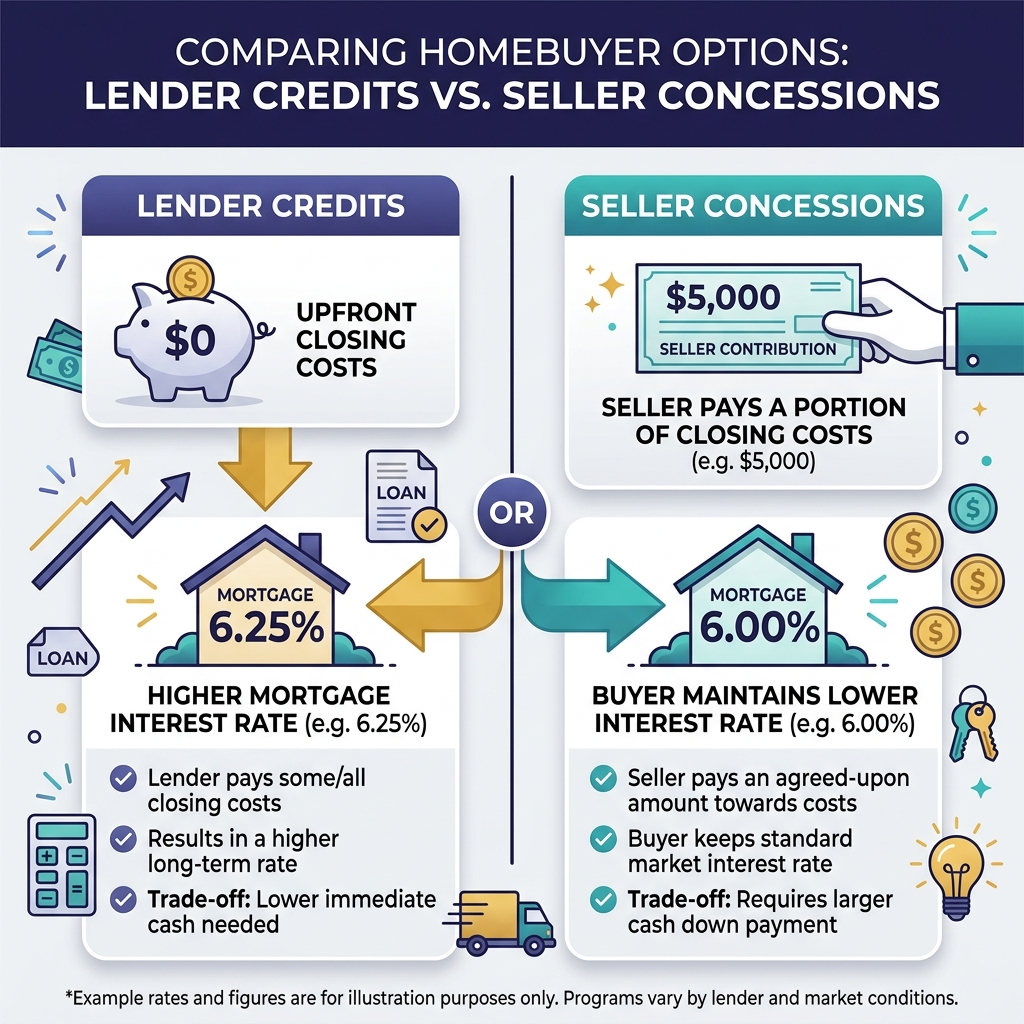

If your closing costs are $8,000, your lender might offer to pay $4,005 of that total. In exchange, they will raise your interest rate by a quarter of a percentage point, for instance, from 6.5% to 6.75%.

This tradeoff means you save money on the day of closing, but your monthly mortgage payment will be higher for the entire life of the loan. This makes lender credits ideal for buyers who are short on cash today but have comfortable monthly incomes, or those who plan to refinance or sell the home within a few years.

- Lowers immediate cash needs at closing

- Lets you purchase a home sooner

- Great if you plan to move or refinance quickly

- Higher interest rate over the loan life

- Increases your monthly mortgage payment

- Costs more in the long run if you hold the loan

Understanding Seller Concessions

Seller concessions are contributions made by the homeowner who is selling the property. To help finalize the sale, the seller agrees to use a portion of the purchase price proceeds to pay for some of your closing costs.

How Seller Concessions Work

Unlike lender credits, seller concessions do not affect your interest rate. If you buy a home for $400,000 and negotiate $6,000 in concessions, the seller will receive $394,000 at closing, and the remaining $6,000 goes to cover your closing costs. Your rate remains at the market level.

To keep the transaction fair, buyers often increase their offer price to cover the concessions. For example, you might offer $406,000 with a request for $6,000 back at closing. This rolls the closing costs into the loan balance.

- No increase to your interest rate

- Keeps monthly payment at base market level

- Lowers immediate out-of-pocket cash requirements

- Must be negotiated during the contract offer

- Harder to get in competitive seller markets

- Limits are capped by loan type regulations

Figure 1: Comparison of lender credits raising interest rates for upfront savings versus seller concessions leaving interest rates unchanged.

Limits on Seller Concessions

Government rules limit the amount a seller can contribute to protect the housing market from inflated valuations. These limits are set as a percentage of the purchase price or the appraised value, whichever is lower.

The rules vary by the type of loan you use. Guidelines for conventional loans are governed by Fannie Mae, which you can read about in detail on the official Fannie Mae Selling Guide.

| Loan Type | Down Payment / LTV | Maximum Contribution Limit |

|---|---|---|

| Conventional Loan | Less than 10% Down Payment | 3% of purchase price |

| 10% to 24.99% Down Payment | 6% of purchase price | |

| 25% or more Down Payment | 9% of purchase price | |

| FHA Loan | Any Down Payment amount | 6% of purchase price |

| VA Loan | Any Down Payment amount | 4% of purchase price |

| USDA Loan | Any Down Payment amount | 6% of purchase price |

Note that VA loans calculate the 4% cap differently. While conventional and FHA limits apply to normal closing costs, the VA limit specifically applies to concessions like paying off buyer credit cards or funding escrow accounts. You can verify VA-specific rules on the Department of Veterans Affairs website.

The Math: How Each Choice Affects Your Budget

Let us look at a real-world scenario to compare the math. Imagine you are purchasing a home with a purchase price of $400,000 using a conventional loan, placing 10% down ($40,000), with a baseline loan amount of $360,000. Your closing costs are estimated at $10,000.

Standard Baseline

Interest Rate: 6.50%

Upfront Closing: $10,000

Down Payment: $40,000

Cash to Close: $50,000

Monthly P&I Payment: $2,275

Lender Credit

Interest Rate: 7.00% (+0.50%)

Upfront Closing: $4,000 (-$6,000)

Down Payment: $40,000

Cash to Close: $44,000

Monthly P&I Payment: $2,395

Costs an extra $120 each month.

Seller Concession

Interest Rate: 6.50% (Unchanged)

Upfront Closing: $4,000 (-$6,000)

Down Payment: $40,000

Cash to Close: $44,000

Monthly P&I Payment: $2,275

Saves $6,000 upfront with no rate increase.

In Scenario B, the lender credit saves you $6,000 at closing, but increases your payment by $120 a month. To find your break-even point, divide the upfront savings by the monthly increase:

If you plan to stay in your home or keep the loan for more than four years, the higher interest rate will cost you more than the upfront cash savings. If you plan to sell or refinance within three years, the lender credit is a highly effective way to keep cash in your pocket.

To run your own numbers and check how changing rates impact your long-term interest costs, explore our interactive amortization schedule tool.

Compare Rate Adjustments and Interest Costs

Plug your loan variables into our amortization scheduler to map out exactly when your premium rate might begin costing more than your initial upfront savings.