This comprehensive glossary defines the 25 essential mortgage terms every homebuyer needs to know, including down payments, loan-to-value (LTV) ratios, private mortgage insurance (PMI), and escrow accounts. Understanding these key concepts will help you communicate confidently with lenders, secure better interest rates, and navigate the underwriting and closing process without costly surprises.

Entering the real estate market is an exciting milestone, but first time buyers often struggle to follow the terminology used by loan officers, underwriters, and real estate agents. Terms like escrow, LTV, and discount points are thrown around daily. Missing the details on these definitions can lead to costly mistakes.

Using a standard mortgage calculator is a great start to estimate monthly expenses, but you must understand the underlying parameters to qualify for a loan. This glossary defines 25 terms you need to know.

01Amortization

The breakdown of your debt paydown over time. Every monthly payment is divided into two parts: paying the accrued interest fee and reducing the principal balance. In the early years, interest fees consume the bulk of the payment; over time, more of your check goes toward the principal. You can examine this progression using our interactive yearly amortization schedule generator.

02Annual Percentage Rate (APR)

The absolute cost of borrowing capital expressed as a yearly rate. Unlike your base note rate, the APR includes closing costs, origination fees, lender underwriting fees, and mortgage insurance. Use the APR, rather than the base interest rate, when comparing loan estimates to identify the most competitive deal.

03Appraisal

A formal valuation of the property conducted by an independent licensed appraiser. Lenders require an appraisal to ensure the home's market value matches or exceeds the agreed purchase price, protecting the bank against lending more than the home is worth.

04Assessed Value

The valuation placed on a home by local municipality tax assessors. This value is used strictly to calculate your annual property tax rate and does not necessarily reflect the current fair market value of the home on the open real estate market.

05Assets

Your total financial holdings (savings accounts, retirement reserves, stocks, and mutual funds). Lenders review your bank records during underwriting to verify that you have sufficient funds for your down payment, closing costs, and post-closing reserves.

06Closing Costs

The administrative and transaction fees required to finalize your mortgage. These typically include lender origination charges, title search fees, title insurance premiums, county recording costs, and home appraisal fees. According to official guidelines from the Consumer Financial Protection Bureau (CFPB), closing costs generally total 2% to 5% of the total loan amount.

07Debt-to-Income (DTI) Ratio

The metric lenders use to assess your capacity to handle a monthly mortgage payment. It measures your total recurring monthly debt obligations against your gross monthly income. To see how DTI limits affect your eligibility thresholds, check our home affordability calculator.

08Down Payment

The cash contribution you make upfront toward the purchase price of the property. Lenders subtract this down payment from the home's total price to determine the remaining mortgage principal balance.

09Earnest Money Deposit (EMD)

A security deposit paid to an escrow company when you sign a home purchase contract. It demonstrates to the seller that your offer is serious. EMD is typically 1% to 2% of the sales price and is applied directly to your down payment or closing costs at final settlement.

10Equity

The portion of the home that you actually own. It is calculated by subtracting your remaining mortgage principal balance from the property's current assessed market value. Equity builds as you pay off the principal and as the home appreciates.

11Escrow Account

A reserve account managed by your loan servicer. A portion of your monthly check is deposited into this account to pay for property taxes and homeowners insurance policies when they come due.

12Fixed-Rate Mortgage

A loan where your interest rate remains constant for the entire duration of your term (commonly 15 or 30 years). This protects you from rising market rates and guarantees a stable monthly principal and interest payment.

13Adjustable-Rate Mortgage (ARM)

A mortgage where the interest rate changes periodically based on benchmark market indexes. ARMs typically feature a lower initial interest rate for a fixed period (such as 5 or 7 years) before adjusting annually, introducing payment variability.

14Interest Rate

The cost to borrow the principal balance, calculated as a percentage. This rate does not include closing costs or other setup charges.

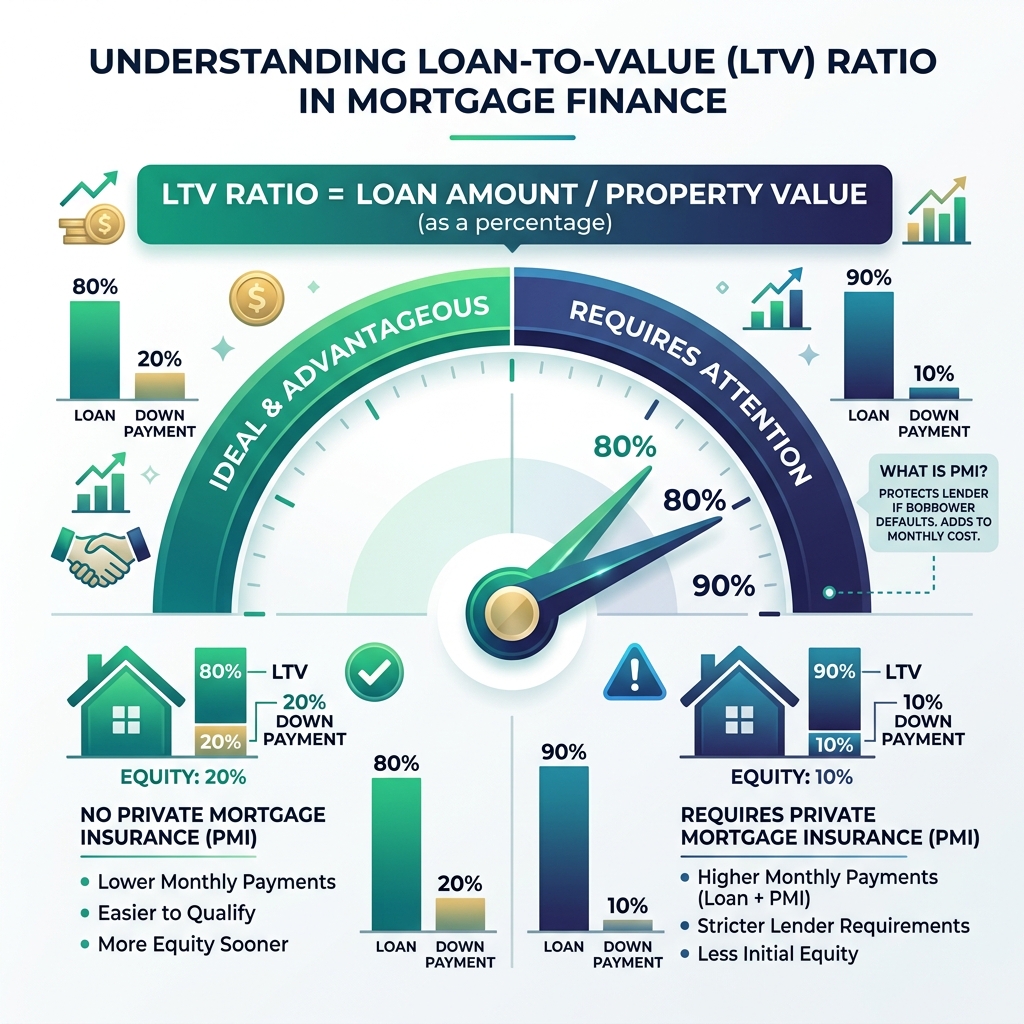

15Loan-to-Value (LTV) Ratio

The ratio lenders use to evaluate default risk. It measures the loan amount against the property's appraised value or purchase price, whichever is lower. A lower LTV ratio represents less risk for the lender.

Figure 1: How LTV shifts based on your down payment size. Reaching an 80% LTV threshold removes Private Mortgage Insurance requirements.

16Mortgage Insurance Premium (MIP)

The insurance premium required for FHA loans. Unlike conventional PMI, MIP consists of both an upfront fee paid at closing and a monthly premium that remains for the entire life of the loan in most cases.

17Origination Fee

An upfront fee charged by lenders to cover the cost of preparing, reviewing, and evaluating your mortgage application. This fee is typically calculated as a percentage of the total loan amount (usually 0.5% to 1%).

18PITI

An acronym representing the four standard components of a monthly mortgage bill: Principal, Interest, Taxes, and Insurance. Lenders assess these four combined costs when evaluating your debt capacity.

19Pre-Approval

A formal evaluation of your creditworthiness by a lender. Unlike a simple pre-qualification, a pre-approval requires verified income and asset records. This shows sellers that a bank is committed to financing your purchase.

20Principal

The actual balance of money borrowed. Any payment applied to your principal directly reduces your outstanding balance. Reducing your principal early lowers your monthly interest charges. You can calculate these compounding interest savings using our early payoff calculator.

21Private Mortgage Insurance (PMI)

An insurance policy required for conventional loans when your down payment is less than 20% of the purchase price. PMI protects the lender in case of default. It does not cover your equity. PMI can be canceled once your principal balance reaches 80% of the original purchase price.

| Feature | Conventional PMI | FHA MIP |

|---|---|---|

| Minimum Down Payment | Typically 3% to 5% | 3.5% |

| Cancellation Policy | Removable at 80% LTV (20% equity) | Usually remains for the entire life of the loan |

| Upfront Fee Required | No (unless chosen as single premium) | Yes (typically 1.75% of the loan amount) |

22Refinancing

The process of replacing your current mortgage with a new one. Homeowners typically refinance to secure a lower interest rate, shorten the loan term, or convert home equity into cash.

23Title Insurance

An insurance policy that protects against financial losses from title defects, ownership disputes, or unpaid property liens. Lenders require a lender’s title policy, while an owner’s title policy is recommended to protect the buyer.

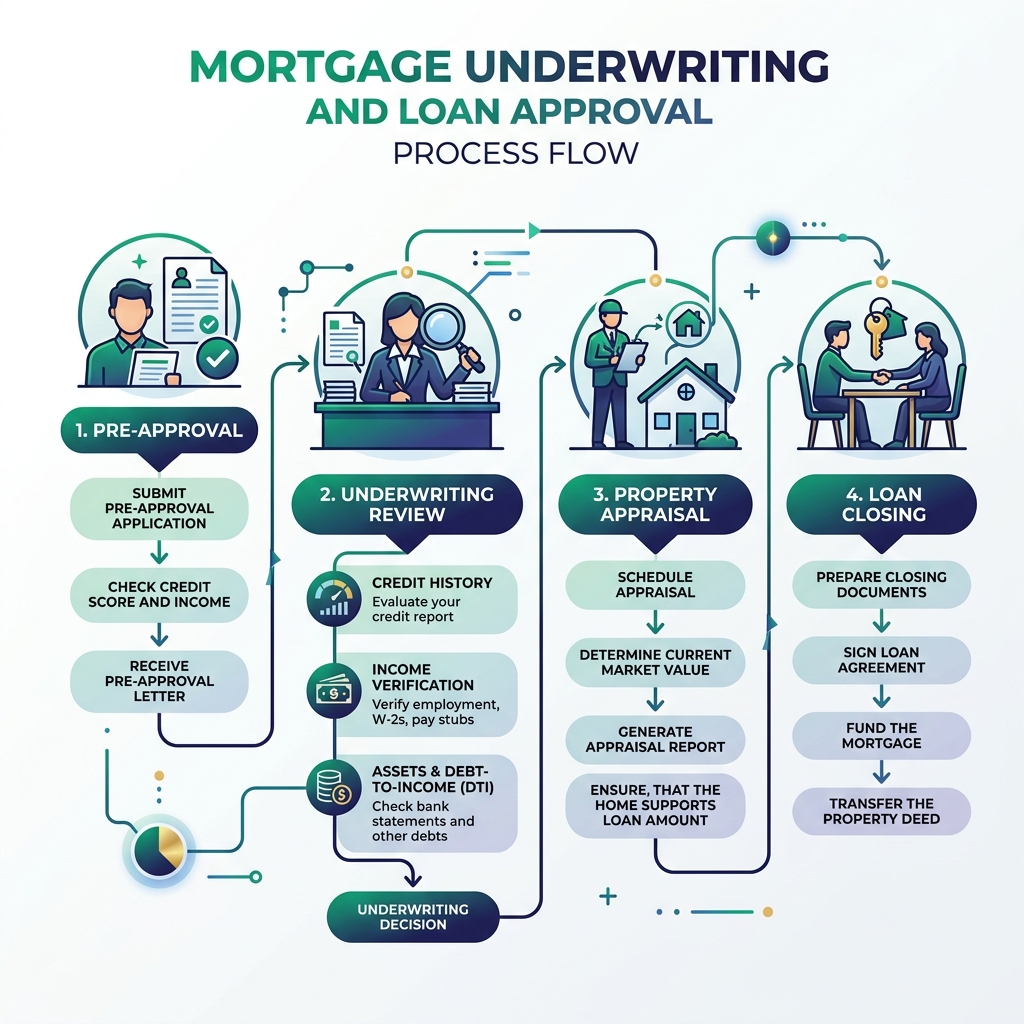

24Underwriting

The review process where a lender evaluates your credit score, income history, and assets to determine your risk of default. The underwriter makes the final decision on whether to approve your loan. According to standard Fannie Mae eligibility guidelines, underwriting acts as the key safety gate in the mortgage lending pipeline.

Figure 2: The step-by-step roadmap from initial pre-approval and financial review to appraisal verification and final loan closing.

25Discount Points

Prepaid interest fees paid directly to the lender at closing. One discount point equals 1% of the loan amount and typically reduces your interest rate by approximately 0.25%, lowering your monthly payment.

The Bottom Line

Understanding these 25 terms changes you from a passive applicant into an informed borrower. Knowing these definitions allows you to evaluate estimates, track closing fees, and plan your down payment. Before starting your home search, establish a clear budget using a calibrated housing tool to protect your long term financial health.

Put Your Financial Pre-Approval Into Action

Connect these dictionary concepts to your real-life numbers. Use our home affordability tool to assess your front-end and back-end debt parameters.