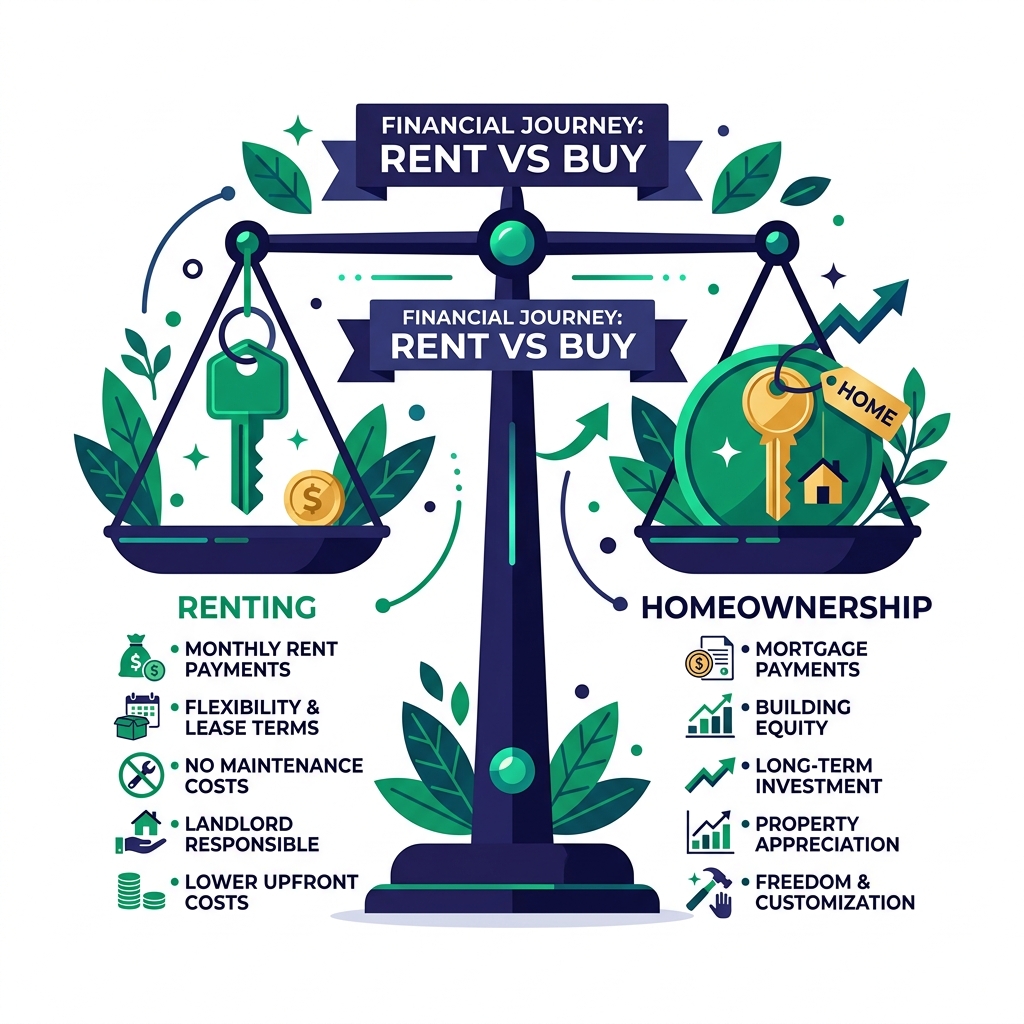

Buying a home is not always the best way to build wealth. Renting is often the smarter financial move when you expect to move within five years, or when investing your down payment capital elsewhere yields higher historical returns. Comparing the transactional and monthly unrecoverable costs of both strategies reveals that renting can serve as an excellent vehicle for wealth accumulation.

For generations, homeownership has been promoted as the ultimate symbol of financial success. The common wisdom is simple: renting is equivalent to throwing money away, while buying a home is always a sound investment. Unfortunately, this binary perspective ignores the actual math of real estate transactions.

In reality, both renting and buying carry significant unrecoverable costs. When you understand how these costs balance against each other, you can use our interactive rent vs. buy cost calculator to model your custom scenarios.

To understand the full spectrum of housing costs, you can also read our deep dive into the hidden costs of homeownership, or study the details of your monthly payment in our guide on how PITI mortgage components work.

The Transaction Cost Hurdle

One of the most overlooked aspects of real estate is the friction of transaction fees. Buying and selling a home requires paying a long list of professionals, government fees, and taxes that do not add any value to the property itself.

Understanding Upfront and Exit Fees

When you purchase a home, you pay closing costs that average 2% to 5% of the purchase price. When you eventually sell the home, you pay real estate agent commissions, transfer taxes, and escrow fees that typically eat up another 5% to 8% of the sales price.

To recoup these transaction costs, your home must appreciate significantly. If you buy a $400,000 home and sell it four years later, you might pay $12,000 in upfront closing fees and $24,000 in selling costs. That means you are down $36,000 before accounting for any maintenance or interest. If you plan to relocate or upgrade within five years, renting is almost always the safer financial option.

The Opportunity Cost of Capital

Every dollar you put into real estate is a dollar that cannot be invested elsewhere. This is known as opportunity cost, and it plays a massive role in long-term wealth building.

Comparing Home Equity vs. Financial Markets

To buy a home, you must lock up a significant lump sum for a down payment. If you buy a $400,000 home with 20% down, that is $80,000 in cash. While that money sits in your home equity, its return is tied to local housing appreciation, which has historically averaged around 3% to 4% annually over the long term.

If you rent instead, you can keep that $80,000 down payment capital fully liquid. By investing it in a diversified stock market index fund, which has historically averaged 8% to 10% annual returns, your compound growth can easily outpace the equity gains of homeownership. This makes renting a viable strategy for building wealth, provided the capital is actually invested and not spent.

Figure 1: The balance of homeownership costs (interest, taxes, maintenance) vs renting unrecoverable costs (rent check and lost investment growth).

The Myth of "Throwing Money Away"

People often compare a rent payment directly to a mortgage payment and conclude that buying is better because you build equity. This comparison is fundamentally flawed because it ignores the unrecoverable costs of homeownership.

Understanding Unrecoverable Costs (The 5% Rule)

When you rent, your rent payment is your maximum monthly housing expense. When you buy a home, your mortgage payment is only the minimum monthly expense. Homeowners face several costs that are just as unrecoverable as rent:

- Mortgage Interest: In the early years of a loan, most of your payment goes to interest, not principal.

- Property Taxes: This is a recurring tax paid to your local government that never disappears.

- Maintenance and Repairs: Home maintenance typically costs 1% to 2% of the home value annually.

- Homeowners Insurance & HOA Fees: Unrecoverable premiums and neighborhood dues.

Financial analysts use the 5% rule to estimate these unrecoverable costs. Multiply your home value by 5% and divide by 12. If you can rent a comparable home for less than that amount, renting is mathematically superior. For a $400,000 home, the unrecoverable cost is roughly $1,666 a month. If you can rent it for $1,500, renting saves you money.

When is Renting the Smarter Choice?

Based on these financial variables, renting is the smarter strategic move in several common scenarios:

- You Plan to Move Soon: If you expect to stay in a city for less than five years, renting protects you from transaction fee losses.

- The Rent-to-Price Ratio is Low: In expensive metropolitan areas, renting is often dramatically cheaper than buying a comparable property.

- You Value Financial Liquidity: Keeping your cash in liquid investment vehicles like stocks allows your portfolio to compound faster.

- You Prefer Predictable Budgets: Renting shields you from the financial shock of emergency repair costs (such as a roof replacement or plumbing failure).

Understanding the housing market requires checking realistic parameters. You can read more about broad market conditions on the official Federal Reserve website, or research mortgage tax implications via the Internal Revenue Service mortgage interest deductions resource.

Run Your Own Rent vs. Buy Analysis

Enter your local rent prices, home values, interest rates, and investment assumptions to calculate exactly which path builds more wealth for your timeline.