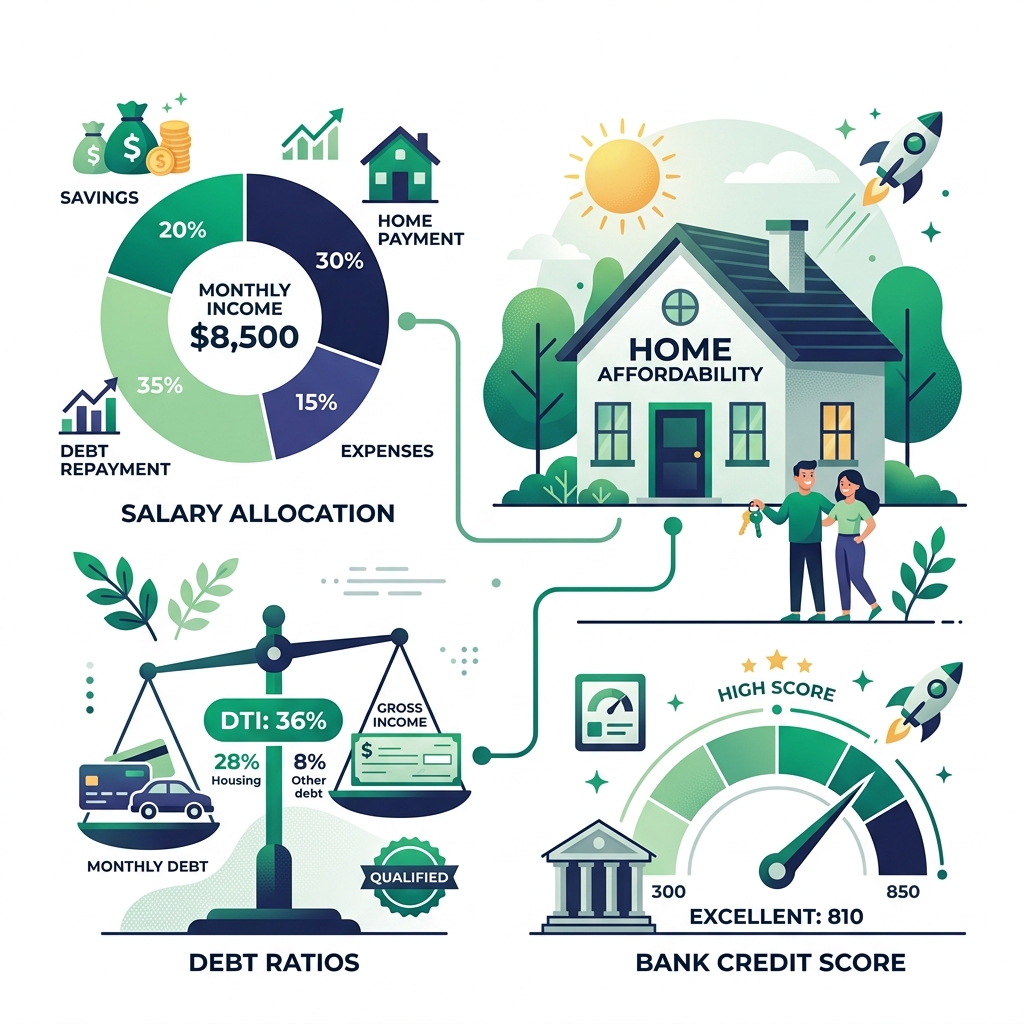

To avoid becoming house poor, calculate your budget based on take-home pay rather than the lender's pre-tax approval limit. Lenders focus on gross pre-tax income, ignoring variables like tax brackets, children, healthcare, and groceries. When you borrow up to your maximum pre-qualification limit, you risk locking yourself into high monthly payments that consume all discretionary cash. Calculate your true limits by accounting for hidden ownership costs, building a six-month reserve cushion, and treating general lending rules as limits rather than targets.

The process of buying a home usually begins in a lender's office. You hand over your pay stubs, tax returns, and bank statements. Within days, you receive a pre-approval letter stating you are cleared to borrow a specific amount.

This number is often surprisingly high. For many buyers, the maximum approval limit represents a monthly payment that would severely stretch their household finances. Moving forward with that budget ceiling can lead straight into a situation commonly known as being house poor. To run a realistic check on your debt limits and play with different scenarios, you can use our interactive home affordability calculator.

Why Maximum Approval Does Not Equal Affordability

Lenders calculate loan eligibility based on gross pre-tax income, using standard debt-to-income (DTI) frameworks such as the 28/36 qualifying guideline. While this math works for a spreadsheet, it is far from real-world budgeting. Gross income does not account for the income taxes that immediately reduce your paycheck, nor does it factor in essential household costs like child care, retirement savings, or utilities.

To research general guidelines on consumer debt, visit the educational resources published by the Consumer Financial Protection Bureau (CFPB), or check housing budget outlines shared by the U.S. Department of Housing and Urban Development (HUD).

Four Steps to Finding Your True Affordability Limit

Avoiding the stress of an oversized mortgage requires a proactive approach. By calculating your housing costs against your net take-home pay, you can establish a safe boundary. Here are four practical guidelines to set your budget:

Budget Off Net Income, Not Gross Pre-Tax pay

Start your calculations with the actual money deposited into your bank account each month. Subtract taxes, health insurance premiums, and retirement contributions first. If you base your mortgage payment on pre-tax figures, you will find yourself short on cash when actual bills arrive.

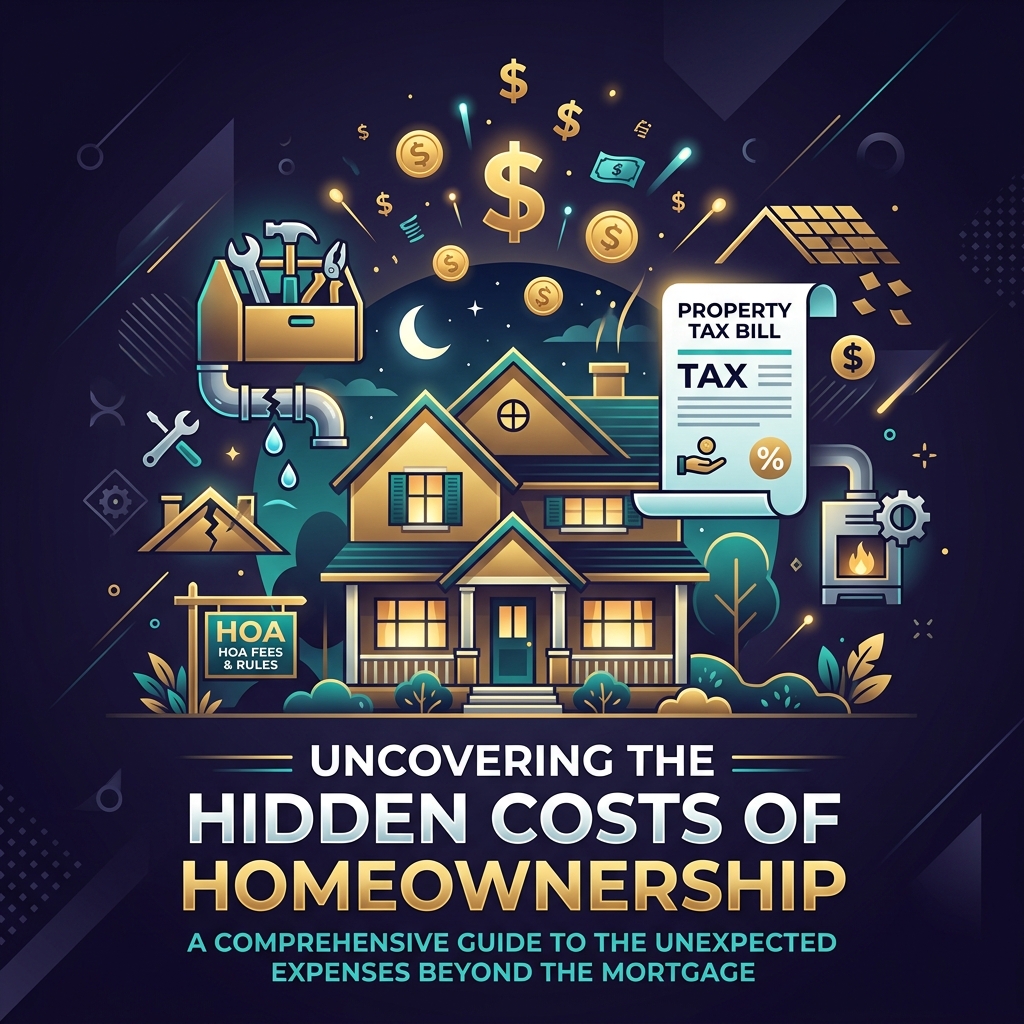

Include the Full Cost of Ownership

Your home loan is only one part of the housing bill. You must account for property taxes, homeowners insurance, HOA fees, and maintenance. In addition, utilities are typically much higher in a house than in an apartment. Factor these hidden expenses into your budget immediately.

Maintain a Six-Month Emergency Reserve

Do not spend your last dollar on the down payment and closing fees. Keep a dedicated cushion in savings to cover home repairs or potential income loss. If you drain your savings account completely to close, a single broken furnace can push you into high-interest credit card debt.

Treat Rule Limits as Ceilings, Not Goals

Standard formulas like the 28/36 rule represent maximum limit parameters. However, you do not have to stretch to these limits. Choosing to buy a home that costs less than your qualifying maximum leaves room for other financial priorities, such as travel, dining, or college funds.

Figure 1: Housing affordability is shaped by multiple non-mortgage variables that lenders omit from debt calculations.

The Long-Term Impact of a Comfortable Housing Budget

When your housing payment takes up a reasonable percentage of your take-home pay, you gain financial peace of mind. You can comfortably manage the hidden costs of homeownership, cover your total monthly PITI mortgage components, build up your retirement assets, and handle unexpected maintenance bills without stress.

Review Your True Home Purchasing Limits

Connect your net details, subtract recurring payments, and define a monthly housing cost that fits comfortably within your take-home pay.